The industrial storage market in California is experiencing significant growth, driven by the increasing demand for energy efficiency, sustainability, and the integration of renewable energy sources. As one of the largest economies in the world, California’s commitment to reducing greenhouse gas emissions and transitioning to renewable energy has created a robust environment for industrial storage solutions. This article provides a comprehensive analysis of the current market landscape, key trends, challenges, and future opportunities in industrial storage within California.

Overview of the Industrial Storage Market

California leads the nation in energy storage deployment, with a focus on both utility-scale and behind-the-meter solutions. The state has set ambitious goals to achieve 100% clean energy by 2045, which has propelled investments in energy storage technologies.

Market Size and Growth Rate

The industrial storage market in California is projected to grow significantly over the next decade. According to recent reports, the market was valued at approximately $1.5 billion in 2023 and is expected to reach around $4 billion by 2030, reflecting a compound annual growth rate (CAGR) of 16%.

| Year | Market Value (in Billion USD) | CAGR (%) |

|---|---|---|

| 2023 | 1.5 | – |

| 2024 | 1.8 | 20% |

| 2025 | 2.2 | 22% |

| 2030 | 4.0 | 16% |

Key Drivers of Market Growth

1. Renewable Energy Integration

California’s aggressive renewable energy targets necessitate advanced energy storage solutions to balance supply and demand. The integration of solar and wind power into the grid requires reliable storage systems to manage fluctuations in energy production.

2. Policy Support and Incentives

State policies such as the California Public Utilities Commission (CPUC) mandates and financial incentives for energy storage projects are driving market growth. Programs like the Self-Generation Incentive Program (SGIP) provide financial support for businesses adopting energy storage technologies.

3. Increasing Demand for Energy Resilience

The growing frequency of power outages due to wildfires and other natural disasters has heightened the need for reliable energy storage solutions. Industries are increasingly investing in battery systems to ensure uninterrupted power supply during emergencies.

Market Segmentation

The industrial storage market can be segmented based on technology type, application, and end-user industry.

1. Technology Type

- Lithium-ion Batteries: Currently dominate the market due to their high energy density and decreasing costs.

- Flow Batteries: Gaining traction for large-scale applications due to their scalability and long cycle life.

- Lead-Acid Batteries: Still used but gradually being replaced by more efficient technologies.

2. Application

- Peak Shaving: Businesses utilize storage systems to reduce peak demand charges.

- Load Shifting: Storing energy during off-peak hours for use during peak demand times.

- Backup Power: Providing emergency power supply during outages.

3. End-User Industry

- Manufacturing: Significant investments in energy storage for operational efficiency.

- Commercial Buildings: Increasing adoption of battery systems for energy management.

- Telecommunications: Utilizing backup power systems to ensure network reliability.

Challenges Facing the Market

Despite its growth potential, the industrial storage market in California faces several challenges:

1. High Initial Costs

The upfront costs associated with installing advanced energy storage systems can be prohibitive for many businesses, despite long-term savings on energy bills.

2. Regulatory Hurdles

Navigating complex regulatory frameworks can slow down project implementation and increase costs. Ensuring compliance with state and federal regulations is essential but can be cumbersome.

3. Technological Limitations

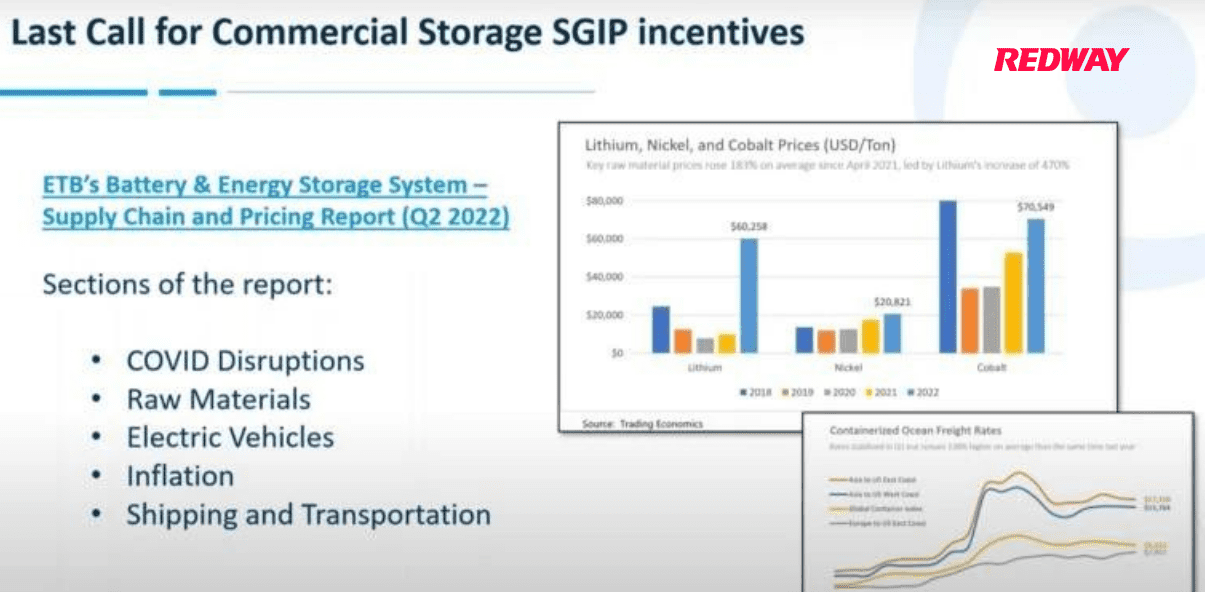

While lithium-ion batteries are prevalent, concerns about their environmental impact and resource availability (e.g., lithium mining) pose challenges for sustainable growth.

Future Opportunities

The future of industrial storage in California looks promising, with several opportunities on the horizon:

1. Innovation in Energy Storage Technologies

Advancements in battery technology, such as solid-state batteries and improved flow batteries, will enhance performance metrics while reducing costs.

2. Expansion of Microgrid Systems

Microgrids that integrate renewable sources with storage solutions are gaining popularity in California’s industrial sector, providing enhanced resilience and efficiency.

3. Increased Collaboration Between Stakeholders

Collaboration among government agencies, private companies, and research institutions can drive innovation and accelerate the deployment of industrial storage solutions.

Conclusion

In conclusion, the industrial storage market in California is poised for substantial growth driven by renewable energy integration, supportive policies, and increasing demand for energy resilience. While challenges such as high initial costs and regulatory hurdles exist, ongoing innovations and strategic collaborations present significant opportunities for stakeholders in this dynamic sector. As companies like Redway Battery continue to innovate within this space by providing high-quality Lithium LiFePO4 batteries tailored for various applications, they play a crucial role in supporting California’s transition towards a sustainable energy future.For customized LiFePO4 battery solutions or inquiries regarding our products designed for wholesale and OEM customers worldwide, contact Redway Battery today for a quick quote!